Giving Tuesday Charitable Discount!

Today is giving Tuesday! Giving Tuesday was apparently created in 2011 and has become a part of the launch-into-holiday weekend that kicks off around thanksgiving and seems to get longer and longer every year… After 5 days of gluttony, it seems the timing is ripe to start thinking about giving rather than consuming!

But just because today is about giving, doesn’t mean that you can’t still get a discount! You probably already understand that charitable contributions can come with tax benefits, but can you confirm if you are getting those benefits or not?

When asked that question, often we will hear answers like, “well, after the Trump tax cuts, we don’t itemize anymore”, or something like “it’s not enough to matter”. There are a handful of other objections, but as advisors, it’s our job to push a step or two further and create intentional strategies to both save money and increase simplicity.

Introducing the Donor Advised Fund (hereby referred to as DAF). DAFs allow you to disconnect the timing of the tax benefits from a charitable contribution with the actual act of donating to a charity of your choice. Let me explain by comparing two examples:

Example 1 (no DAF): Over the next 3 years, let’s say that you donate 5k/year. Depending on your other itemized deductions, you may or may not be able to get any real benefit for having made the donation, but you will track this as a 5k donation each year.

Example 2 (with DAF): You put 15k into the DAF in year 1 and receive full benefit for the donation in the first year. That money stays invested in an account directed by you, and you can direct donations any time that you choose (no ongoing tax benefit for donations out of the DAF).

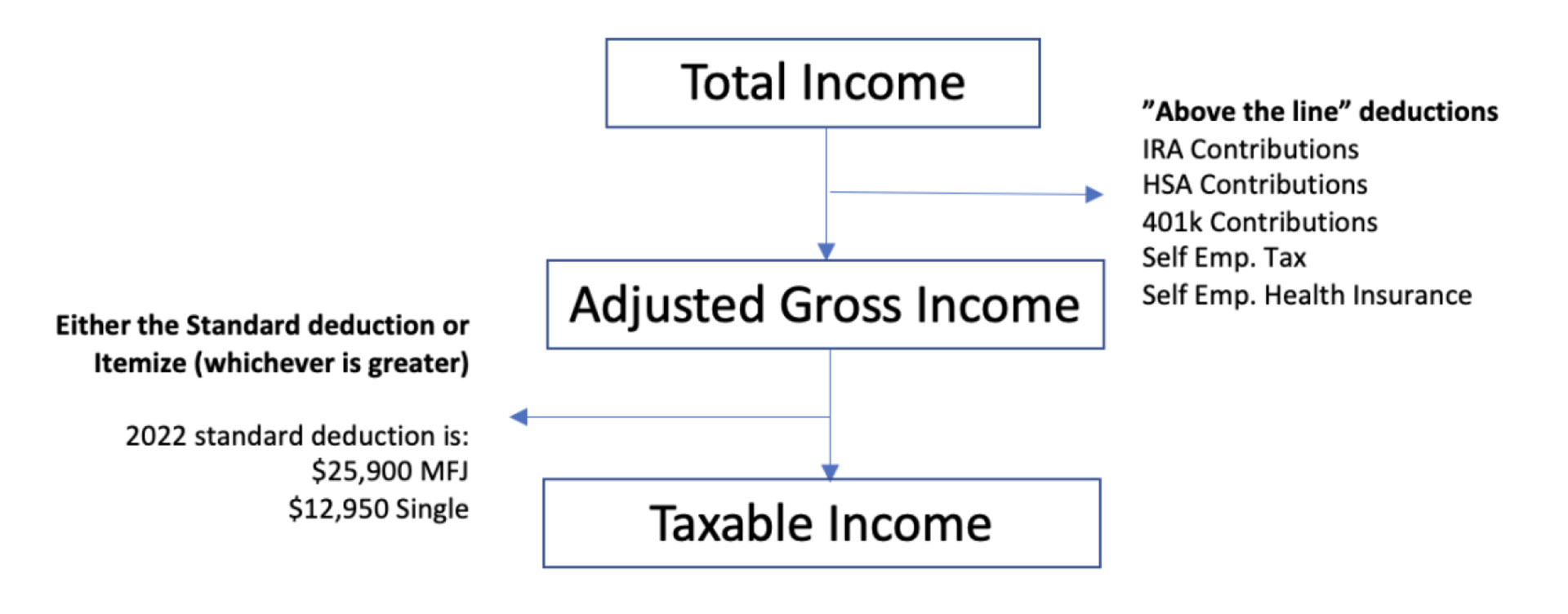

To understand the power of this benefit, it’s important to grasp how a personal tax deduction works… (the following example is a simple way of breaking it down…

As you can see, for a married couple, you really do not benefit from itemizing until you have at least $25,900 of itemizable expenses. Common itemizable expenses include mortgage interest, state and local taxes (capped at 10k currently), healthcare expenses (subject to an income floor), and charitable donations.

So, let’s go back to the prior example of 5k/year donation. Let’s assume that this person is married, and has 10k of state and local taxes, plus another 10k of mortgage interest (20k of itemizable expenses before charitable). Their 5k/year is only moving the needle to 25k, which is still less than the standard deduction…. Still no tax benefit.

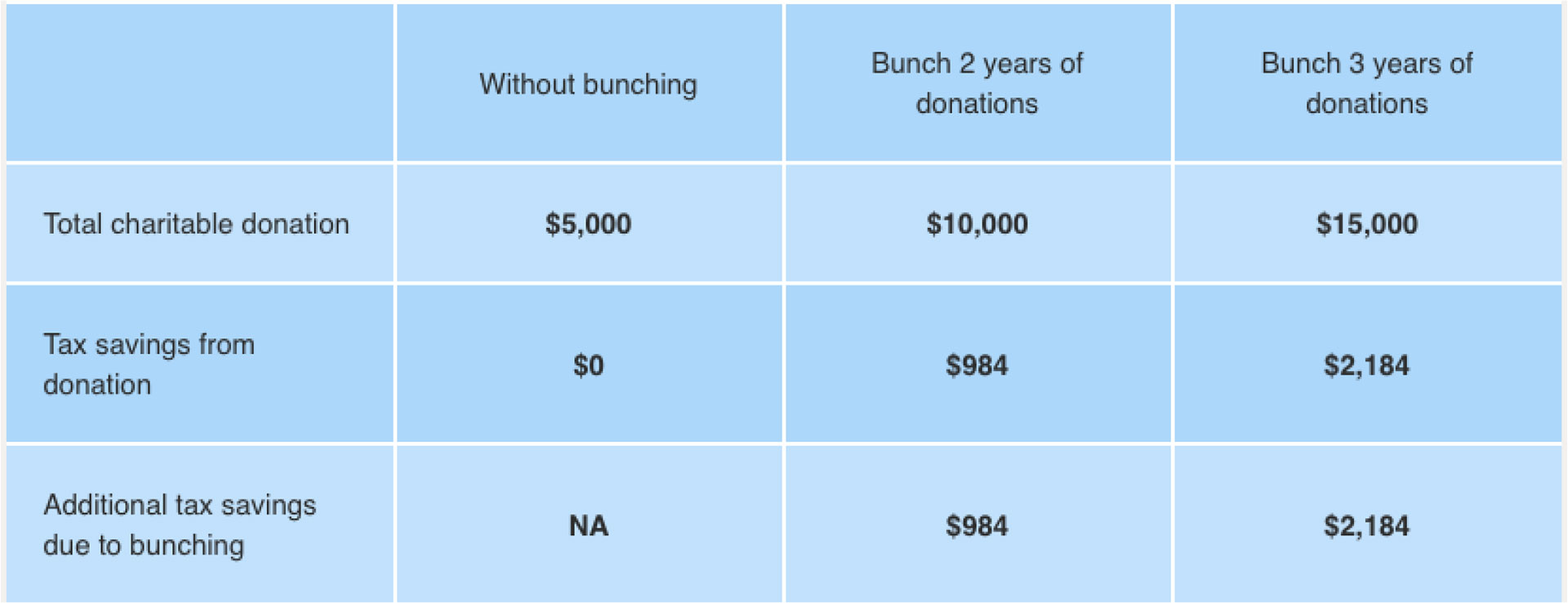

By moving the entirety of the donation into the first year, that 50k can all be added to itemizable expenses. Rather than getting potentially no deduction over 10 years, the person would have 70k (20k + 50k) of itemized expenses in year 1!

Here is a chart to show the benefit of this scenario assuming this married couple is in the 24% tax bracket:

These effects can be taken even further when coupled with the timing of a high tax year vs a low tax year. It can even be funded with appreciated stock which allows you to avoid paying tax on a gain that may otherwise be taxed, adding even more benefit. Furthermore, if you really love that appreciated Apple stock that you just donated, you can repurchase the stock and establish a higher cost for the future.

So, now that the case is made for why it can be more optimal to use a donor advised fund, let’s touch on why it can be simpler…. When it comes to filing your taxes, have you ever had to compile receipts to track what donations were made? Have you ever added the complexity of donating appreciated stock to different charities? These things are simple in concept but can be administratively complex in application. The DAF eliminates this by creating one tax form to track the entire donation, and it links to your brokerage firm for seamless transfer.

Disclosure: This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop and are purely opinions