“New Year, New Market?”

Something has changed…

In our last letter, we discussed 2022 and why it was a tough year for markets. Both stocks and bonds saw losses for the year as the Federal Reserve embarked on a historic sequence of rate hikes. But as we have moved into 2023, we’ve seen a material shift to the currents within markets. We can (and will) speculate the reasons for this, but looking at the data, the shift is clear. We’re (at least for the moment), back in growth mode.

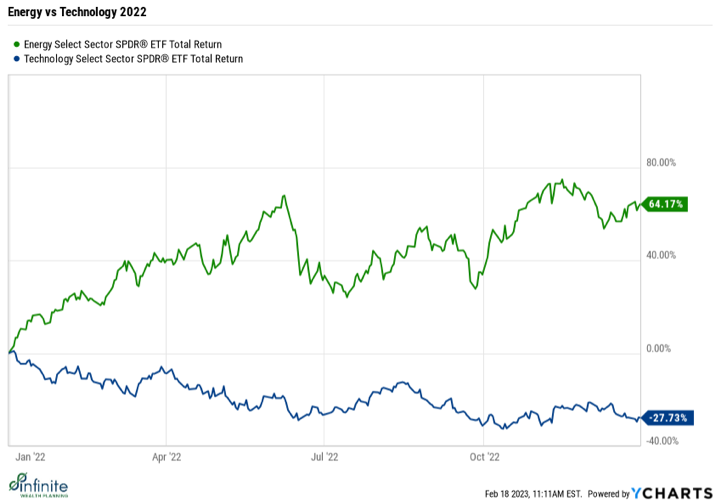

For some context, here’s energy vs technology performance in 2022. Energy stocks were up 64% with technology companies down -28%!

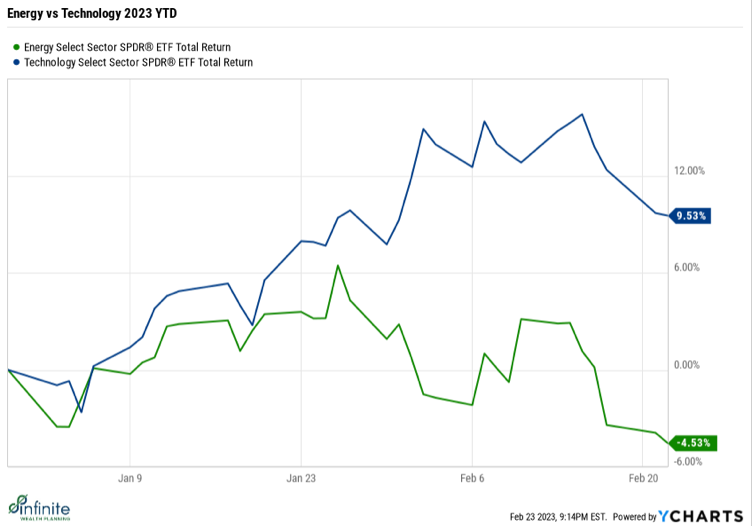

Comparing that to the beginning of 2023, we’ve seen a massive reversal to this trend. Energy stocks are down over 4% with technology up more than 9%!

And other more speculative asset classes are rallying as well. Cryptocurrencies are hot again, with Bitcoin and Ethereum back above levels prior to the FTX fallout. Speculative technology stocks are off to the races this year as well, with the ARK Innovation ETF up roughly +30% this year.

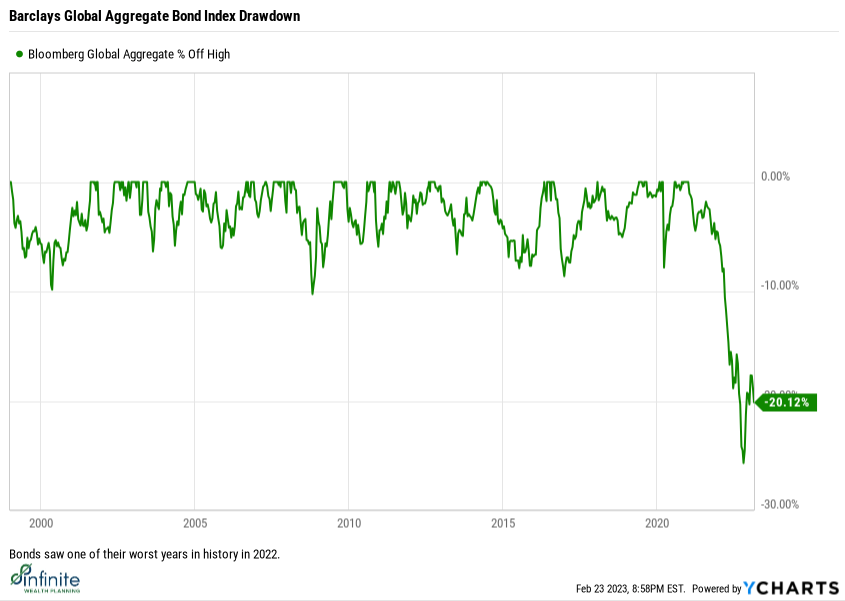

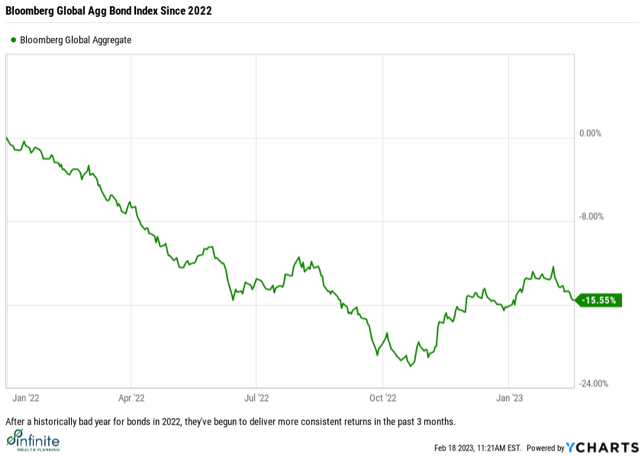

Even bonds have begun to turn around. After a historically bad year in 2022, bonds have been trending higher over in the past few months.

Lastly, here is a chart of the market. In 2022, we made a sequence of lower highs and lower lows as we were in a downtrend. Since October, we’ve started to make higher highs and higher lows. The lines on the chart represent the 50- and 200-day moving averages, which show the average short term price vs long term price. When short term prices start to outweigh long term prices, we see the 50-day moving average cross above the 200-day, which is a positive indicator that momentum is shifting from negative to positive.

Clearly, something has changed.

Now, is the shift here to stay? I had an old friend and colleague who used to say, “that’s something smart people could argue about”. Meaning, that there are valid arguments to both sides. Ultimately, that is what makes a market! Today, there is so much information being processed into the market so quickly, thinking that anyone might have a significant leg up without having non-public knowledge is hard to accept.

… So, what information are we processing? What’s different now?

We believe that the market has started to work redirect its focus from inflation to the consumer economy. We’ve now seen 7 sequential months of data where inflation has fallen, and investors seem to believe that the Fed has what it takes to keep inflation down.

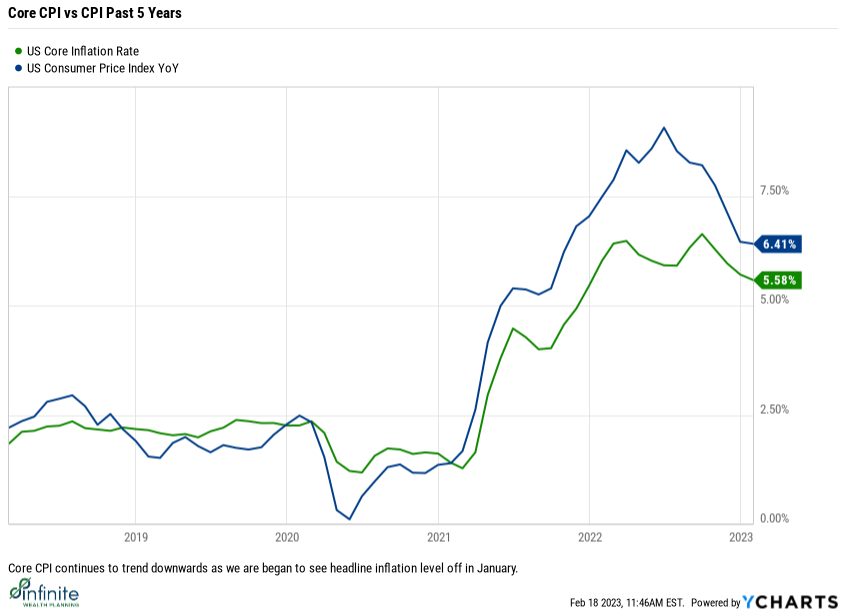

Check out “core” inflation (CPI ex food and energy) compared to the CPI headline… The fed tends to rely on core as a key inflation measure as the price of food and energy can be volatile (think egg prices in Jan 2023). Even with CPI leveling out with the recent Jan release, Core CPI continues to drop Y/Y.

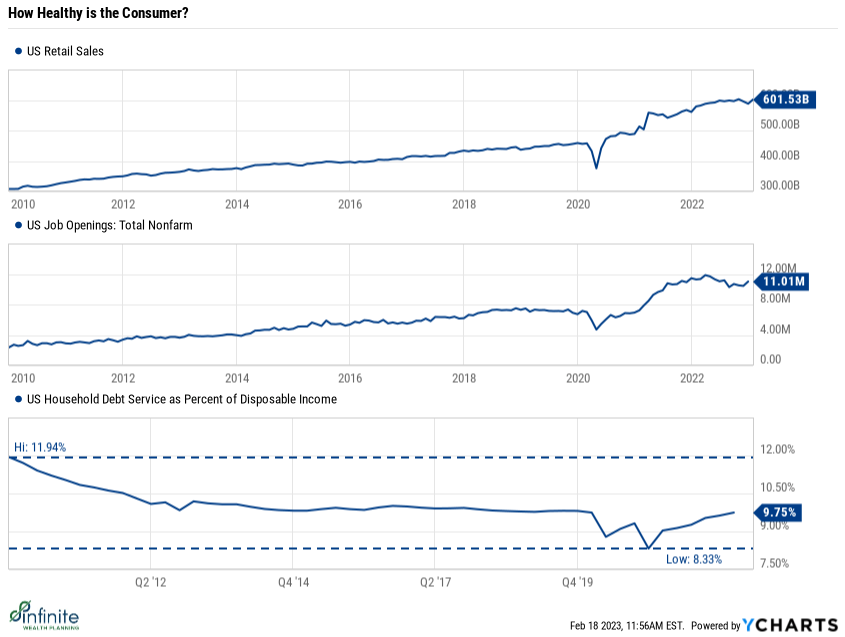

In December, we started to see a drop in some of the economic data. Retail sales and job openings were beginning to trend lower. Fast forward to January, and we’ve seen that trend begin to reverse as the data has started to re-accelerate.

We believe that this will continue to be a driver of the markets. Whereas last year the inflation numbers were the key to market directionality, this year we may start to focus back on the US consumer and the possibility of a “soft landing”.

This year is going to be a year of balance. We will likely find out this year how close the Fed has come to “threading the needle” of killing inflation without killing the economy. For now, the strength in the short-term data is something to be cheered. There does come a point, though, where too much of a strong economy leads to the capacity for more inflation, which drives the economy further into a slump.

We believe that the bull and bear case for the market are these:

- Bull Case: the economic data continues to be resilient, the consumer stays strong, and we continue to see inflation trend lower on in 2h 2023. This is the ideal scenario as we would have a fundamentally strong consumer and reducing inflation.

- Bear Case: Essentially, the bear case is if the “balancing” we are working to achieve now falls apart… If the consumer is too strong, the inflation could be higher than expected, causing the fed to push rates higher for longer. On the other hand, if the consumer is too weak, inflation will likely fall as we potentially face a recession scenario.

For this reason, we believe 2023 will be a year of weighing good economic data and good inflation data, hoping to stay in the “goldilocks zone”.

Advisory services offered through National Wealth Management Group, LLC, a Registered Investment Adviser. This information is intended for educational purposes and is not intended as a recommendation to buy or sell securities. Investing involves risk. Before investing, you should consult with a financial advisor to determine how a specific investment strategy fits your personal goals and objectives.