The pandemic clearly made a large impact on all different parts of the economy. Seldom in history is there an event that makes such an impact both on a personal level (in terms of changing tastes, preferences, and habits), and on an economic level (with historic levels of government stimulus followed by a significant amount of inflation).

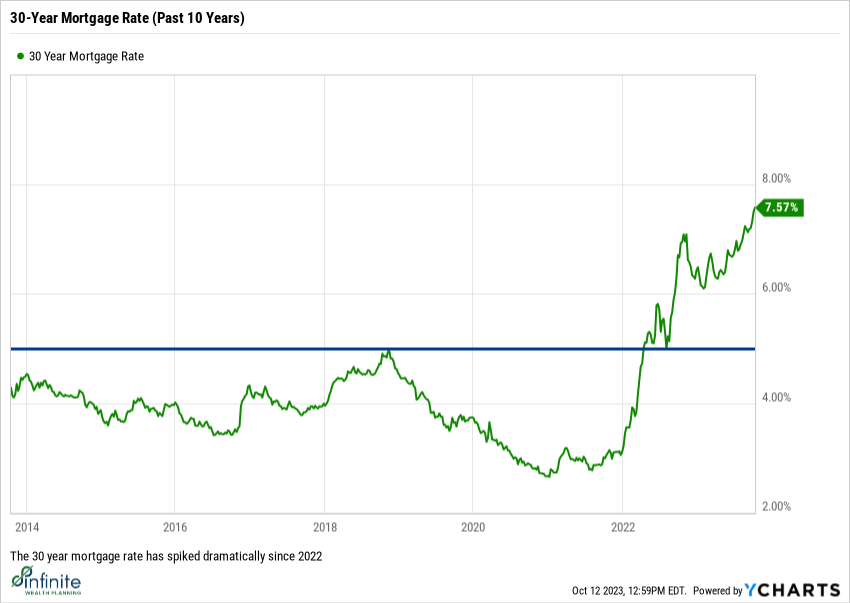

Because of these two things together, there have been significant dislocations in certain markets. One example is real estate, where single family homes and multifamily apartments have seen significant appreciation as people shift their time and energy to their personal residences. And the cost to own these homes isn’t the same for everyone. While some people were able to lock in historically low rates over the last few years, others are still on the sidelines waiting to buy a house.

So, what do you do if you are in the market to buy a house? With low supply and high interest rates, is it the right time to step into home ownership? Or is it better to wait until things “settle down”? This is one of the most common questions that we get from clients today. Here are a few things to consider when it comes to today’s higher interest rate mortgages:

- Remember that the house is not your mortgage. While you may own the house for 20+ years, the mortgage may be temporary if you are to refinance at some point in the future. When rates are high, it’s important to plan to be able to be flexible, meaning that while you should be prepared to pay the mortgage for the full term, but you may have a plan of refinancing when it makes sense.

- Get multiple loan quotes. No, the rate that you are quoted is not the same rate that you’d get at other places. Each institution will have a different appetite for different types of loans, and thus the rates will change depending on who the potential lender is. It’s important to shop a few options to make sure that you are getting favorable terms. With higher rates, some firms are even offering additional incentives like free refinances in the first 5 years or added money towards closing costs. Additionally, multiple credit pulls for the same purpose over a short period of time is looked at as a single credit pull by the credit bureaus, so you don’t have to worry about hurting your credit score in the process.

- Consider shorter interest rate terms. When you get a mortgage, there are a variety of different rate options to choose from. The one that most are familiar with is the 30-year mortgage, where your rate is guaranteed for the full 30-year term of the mortgage, but there are also mortgages called Adjustable-Rate Mortgages (or ARMs for short). These mortgages still require 30 years of payments, but only guarantee an interest rate for limited period of years. Because you as the borrower take on the uncertainty of future interest rates, your current rate is generally lower to compensate.

- Understand the concept of paying “points”. Often when you go to finalize a mortgage, the broker may offer you a loan option that allows you to “buy down” your interest rate. What you are doing in this case is exchanging a lump sum of money up front for a lower rate over time (and thus a lower monthly payment). This can be a great option if you plant to keep the mortgage for a long time, with more time to capture the monthly savings. It’s important to note that if you spend money to buy down your rate and then refinance the loan later on, you will not get the closing costs back. For this reason, if you expect that you might not have the mortgage for a lengthier period (whether you plan to refinance or move), it may not make sense to sink money into lowering your long-term rate.

- Consider options before paying down your principal. Though it can sound expensive to have a 7% loan, that loan may be significantly cheaper if it’s refinanced to 5% in the next handful of years. Once the money has been put into the house, it’s much harder (and more expensive) to get it back out. While it can feel good to have a lower mortgage balance, it’s also important to keep money in savings and investment accounts to cover unexpected needs. If that money is in the house, the only way to get it out is to take another loan of some sort, and this is not always in your control.

In addition, besides the mortgage itself, it’s important to remember that there are additional costs to owning a house. Between property taxes and maintenance, you may find that the true cost is higher than you expected. Remember, when you pay rent, the rent payment is your maximum monthly payment. With a mortgage, the monthly cost is your minimum payment. Don’t forget to plan for some cushion in addition to the monthly payments.

Ultimately, a house is less of an investment decision and more of a lifestyle decision. By having a financial plan in place and being confident that you can afford the house that you are buying, we believe that you should be in the house that serves your needs as opposed to the one with the cheaper mortgage. A lot of people are nervous to pull the trigger on buying right now for fear of a higher rate, but decisions in life can’t all be made around interest rates. By approaching these decisions thoughtfully, you can avoid wasting money around the edges, while focusing on what’s most important.